Blog

Can I Trade My Car During Chapter 7 Bankruptcy in Georgia

So, you’re in the middle of a Chapter 7 bankruptcy and your car is on its last legs. The big question is, can you trade it in?

The short answer is yes, but it’s not as simple as heading down to the dealership. Once you file for bankruptcy, a legal shield called the “automatic stay” goes up, freezing all your assets—including your vehicle. Trying to trade it in without the court's blessing is a huge misstep that could put your entire case at risk.

The Court Approval Rule for Vehicle Trades

Think of your Chapter 7 filing as creating a new legal entity called the bankruptcy estate. Everything you own now belongs to this estate, and a court-appointed trustee is in charge of managing it. Their main job is to make sure your creditors get a fair shake. Since your car is an asset of the estate, you no longer have the authority to sell, trade, or give it away on your own.

To make a move like trading in your vehicle, your attorney must file a formal motion with the court. A bankruptcy judge has to sign off on it, giving you a court order that greenlights the transaction. This process makes sure everything is above board and doesn't shortchange your creditors. For instance, trading a paid-off car for a brand-new one with a hefty loan could look like you're trying to hide a valuable asset from the trustee.

Why Is Court Approval Non-Negotiable?

Trying to sidestep the court is a recipe for disaster. The trustee has the power to unwind the deal, which could leave you without your old car and the new one. Even worse, a judge might see an unauthorized trade as an act of bad faith, which could lead to penalties or even the dismissal of your bankruptcy case.

The bottom line is this: the value in your bankruptcy estate must be protected for your creditors. Any car trade has to show that it either helps the estate or, at the very least, doesn’t hurt it.

This rule holds true even if your car's equity is fully protected by Georgia's bankruptcy exemptions. The court and trustee still need to confirm that the new vehicle and any new loan terms also fall within your allowed exemptions. This is exactly why you need to talk to your attorney before you even think about visiting a car lot. It's not just a good idea—it's essential for protecting your assets and your chance at a fresh start.

To make it crystal clear, ignoring these rules comes with serious consequences. Here's a breakdown of the legal hurdles and risks you'd be facing.

Key Risks of Trading a Car in Chapter 7 Without Approval

This table summarizes the most critical risks and legal hurdles you face when attempting to trade a vehicle during an active Chapter 7 bankruptcy case.

| Legal Factor | What It Means for Your Car | Potential Consequence |

|---|---|---|

| Automatic Stay Violation | The automatic stay freezes all assets. Trading the car is an illegal transfer of estate property. | The trustee can undo the entire sale (called avoidance), leaving you with nothing. |

| Bankruptcy Estate Property | Your car belongs to the estate, not you. Only the trustee or a court order can authorize its sale. | You could face sanctions from the court, including fines or other penalties. |

| Trustee's Avoidance Powers | The trustee can legally reverse any unauthorized transaction made after you filed. | You may lose both the old car and the new one, plus any down payment you made. |

| Bad Faith Determination | A judge may view the unauthorized trade as an attempt to hide assets or defraud creditors. | Your entire Chapter 7 case could be dismissed, leaving you with all your old debt and no protection. |

As you can see, the risks are just too high. The proper legal channels are there for a reason—to ensure a fair process for everyone involved, including you. Always work with your attorney to get the necessary approvals before making any moves.

Why Your Car Becomes Part of the Bankruptcy Estate

When you file for Chapter 7 bankruptcy, something crucial happens the very second your case is filed. All of your property—your home, your bank accounts, and yes, your car—is legally swept into something called the bankruptcy estate.

Think of the estate as a temporary holding company created by the court. At that moment, you no longer have complete control over those assets. Instead, a court-appointed official known as the bankruptcy trustee steps in to manage everything on behalf of your creditors.

This is the single biggest reason you can't just decide to trade in your car during a Chapter 7 case. From the moment you file, the vehicle legally belongs to the estate, not to you. Any move you make with that car, whether it’s selling it or trading it in, requires the trustee's explicit consent and the court's permission.

The Trustee's Role and the Concept of Equity

The trustee's main job is to figure out if there are any non-exempt assets they can sell off to pay back a piece of what you owe. When it comes to your car, the trustee isn't interested in the car itself. They're interested in its equity.

Equity is the number that matters most here. It's simply what your car is worth on the market, minus what you still owe on the loan.

Here's a quick example:

- Vehicle's Fair Market Value: $15,000

- Remaining Loan Balance: -$10,000

- Your Equity: $5,000

That $5,000 is what the trustee sees as a potential asset for the estate. If that amount isn't protected by a legal tool called an exemption (which we’ll get into next), the trustee could sell the car, pay the lender their $10,000, and use the leftover cash for your creditors.

This is exactly why an unauthorized trade-in is such a huge problem. If you trade a car with $5,000 in equity for a new one with little or no equity, you've essentially vaporized an asset that belonged to the estate. The court takes that very seriously.

Because the car and its equity are now property of the estate, you lose the right to make decisions about it on your own. Trying to trade it in is like an employee trying to sell company equipment without permission—the transaction would be invalid, and it would come with some pretty serious consequences for your bankruptcy case.

Understanding this is the first step. Your car is no longer just your car; it's an asset in a legal estate under the court's watch. Every decision has to go through the proper channels—your attorney, the trustee, and the judge—to keep your case on track for that financial fresh start.

How Georgia's Exemptions Protect Your Vehicle

When you file for bankruptcy, your car becomes part of what's called the "bankruptcy estate." But that doesn't mean the trustee automatically gets to sell it. The single most important tool you have to keep your car is an exemption.

Think of exemptions as a legal shield. They're designed to protect essential property—like your car—so you can continue to work and live while getting a fresh start. Whether the trustee can even touch your vehicle comes down to how these exemptions apply.

Calculating Your Car's Protected Equity

It all boils down to some pretty simple math: comparing your car's equity to Georgia's exemption limits. Equity is just the difference between what your car is worth (its fair market value) and what you still owe on the loan.

Here's what Georgia law lets you protect:

- Motor Vehicle Exemption: You can shield up to $5,000 in equity in one car.

- Wildcard Exemption: Georgia also gives you a flexible "wildcard" exemption of up to $1,200 that you can apply to any asset you choose, including your car.

A single person filing for bankruptcy can protect up to $6,200 in vehicle equity. If you're married and filing together, you can double that, potentially protecting up to $12,400 in equity across one or more vehicles. To get the full picture, you can check out our in-depth guide on Georgia bankruptcy exemptions explained.

Crucial Takeaway: If your car's equity is completely covered by your available exemptions, the trustee has no interest in it. It has no value for the bankruptcy estate, and you're free to handle it through other options like reaffirmation or redemption.

Two Scenarios Showing Exemptions in Action

Let’s look at how this plays out in the real world.

Scenario 1: The Fully Protected Car

Imagine your car is worth $12,000, and you owe $8,000 on the loan. That leaves you with $4,000 in equity ($12,000 – $8,000).

Since that $4,000 is less than Georgia's $5,000 vehicle exemption, your car is 100% protected. The trustee can't get any money from it for creditors, so they will "abandon" their interest, and the car remains yours to deal with.

Scenario 2: The Car with Non-Exempt Equity

Now, let's flip the numbers. Your car is worth $15,000, but you only owe $2,000. This gives you $13,000 in equity.

You can apply your $5,000 vehicle exemption and your $1,200 wildcard, for a total of $6,200 in protection. But that still leaves $6,800 of non-exempt equity ($13,000 – $6,200). That unprotected value is an asset the trustee will want to liquidate to pay your creditors, putting your car on the chopping block.

If your car is fully exempt, trading it in is often possible with the court's permission. But there's a catch: the new car you get must also have equity that fits within your exemption limits. If it doesn't, the trustee could seize the unprotected portion of its value.

Choosing the Right Path for Your Auto Loan

Before you can even think about trading in a car during a Chapter 7 bankruptcy, you have to deal with the existing loan. When your car is financed, the bankruptcy code gives you three main options for handling that debt. Each choice sends you down a different financial road and directly impacts whether you can keep or replace your vehicle.

Making this decision is the critical first step. It defines what happens next with your lender, the car, and the debt tied to it.

Understanding Reaffirmation

The most common route people take is reaffirmation. Think of it as hitting the "un-pause" button on your car loan. You sign a new, legally binding agreement with the lender, promising to keep making payments just like you were before you filed for bankruptcy.

In return, you get to keep the car. The most important thing to remember here is that this debt is not discharged with the rest of your debts. If you fall behind on payments down the line, the lender can still repossess the car and even sue you for the remaining balance. Your bankruptcy won't protect you from that.

Exploring Redemption

Your second option is redemption. This is a powerful but much less common strategy, mostly because of the upfront cash required. Redemption lets you buy your car from the lender for its current fair market value, no matter how much you actually owe on the loan.

For example, let's say you owe $12,000 on your car, but its current market value is only $7,000. Redemption allows you to pay the lender a single lump sum of $7,000 to own it free and clear. The other $5,000 of debt gets wiped out in the bankruptcy. The biggest hurdle, of course, is coming up with that lump sum of cash while you're in the middle of a bankruptcy case.

The Path of Surrender

Finally, you can choose to surrender the vehicle. This is usually the simplest path if the car is unreliable, has mechanical issues, or the loan is just too expensive. You voluntarily give the car back to the lender, and the entire remaining loan balance gets wiped out as part of your bankruptcy discharge.

Surrendering the vehicle completely severs your financial ties to it. You walk away with no car and no debt, giving you a completely clean slate to figure out your next transportation needs.

To help you decide which path makes the most sense for your situation, here's a quick comparison of the three main options for your auto loan.

Comparing Your Auto Loan Options in Chapter 7

| Option | What It Means | Best For… | Key Drawback |

|---|---|---|---|

| Reaffirmation | You sign a new contract to keep paying the original loan. | Keeping a reliable car with a reasonable loan balance. | The debt is not discharged; you're still on the hook if you default later. |

| Redemption | You buy the car outright for its current fair market value in a lump sum. | People with "upside-down" loans who can access a lump sum of cash. | Finding the cash for the lump-sum payment is very difficult. |

| Surrender | You give the car back to the lender and walk away from the debt. | Getting out of an unaffordable loan or getting rid of an unreliable car. | You will be left without a vehicle and need to find other transportation. |

Each of these choices has significant consequences, so it's a decision best made after a thorough discussion with your bankruptcy attorney. They can help you weigh the pros and cons based on your car's value, your loan terms, and your overall financial picture.

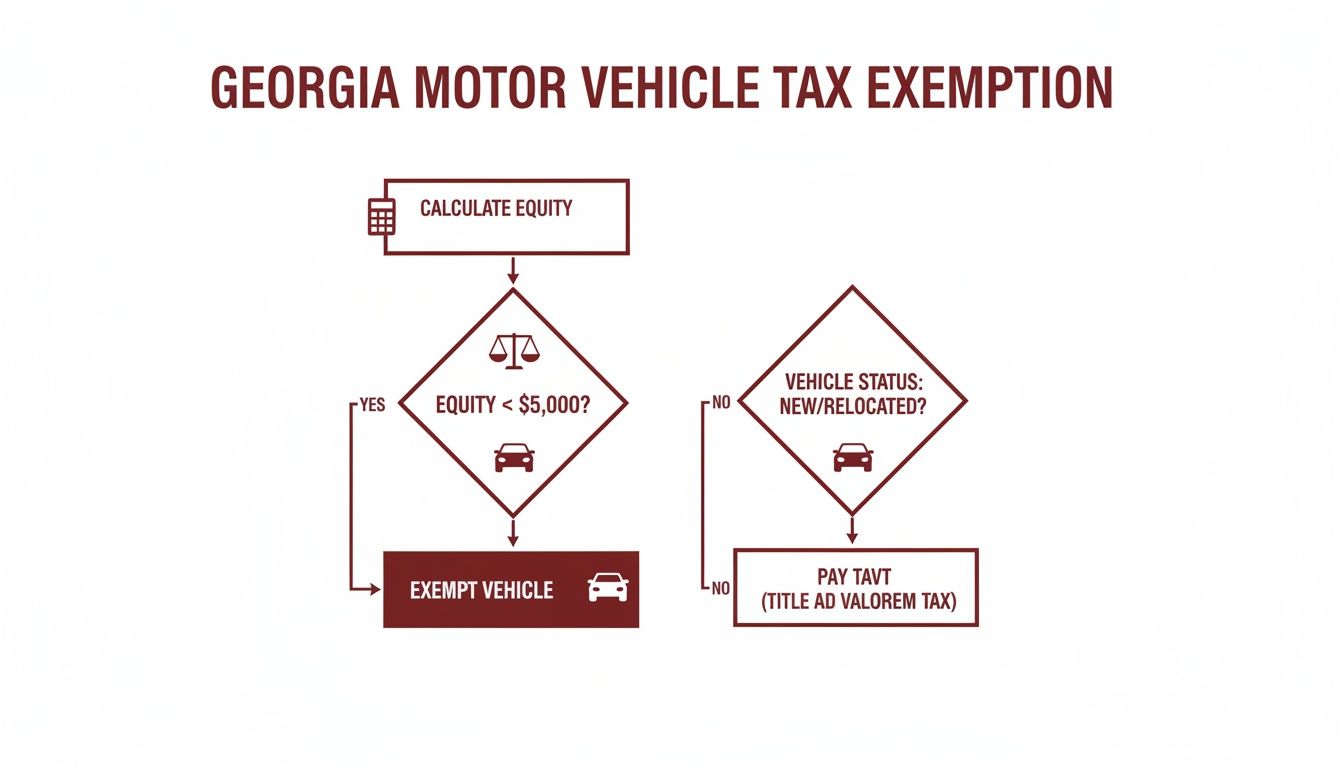

This flowchart helps visualize how your car's equity and your ability to protect it fit into the bigger picture of these decisions.

As the chart shows, you first need to figure out how much equity you have and whether Georgia's exemptions protect it from the trustee. Once you've chosen one of these three paths for the loan, you and your attorney can start exploring the possibility of a court-approved trade-in.

The Official Process for a Court-Approved Car Trade

So, you’ve decided you absolutely need to trade in your car during your Chapter 7 case. Now what? You can’t just walk onto a dealership lot and start signing papers. Trading a car after you’ve filed for bankruptcy is a formal court procedure, not some casual negotiation with a sales manager.

Following the proper legal steps is the only way to make sure the deal is valid and your bankruptcy case stays on the right track. This whole process lives and dies with your bankruptcy attorney. They're your guide and your advocate, making sure every move you make is by the book.

Filing a Motion to Sell or Trade

The first thing your attorney will do is draft a legal document called a Motion to Sell/Trade Property. This gets filed directly with the bankruptcy court. Think of it as a formal request asking the judge for permission to go ahead with the trade. It’s not just a simple form—it’s a legal argument.

Your attorney has to clearly explain why this trade is necessary and show that it either helps your bankruptcy estate or, at the very least, doesn't hurt it. A strong motion will usually include a few key things:

- Proof of Necessity: Evidence that your current car is unreliable, unsafe, or on its last legs. Think mechanic repair quotes or diagnostic reports.

- Financial Justification: A breakdown showing the new car and its financing terms are reasonable and, most importantly, affordable for you.

- Equity Analysis: A clear comparison showing that any equity in the new car will still fall within your allowed Georgia exemption limits.

You essentially have to prove to the court that you're making a responsible financial decision, not just trying to get a flashy upgrade while your debts are being wiped out.

Trustee and Creditor Review

Once that motion is filed, it’s not an automatic approval. The bankruptcy trustee and your creditors get a chance to look it over. They typically have around 21 days to file an objection if they think the trade is a bad idea or harms their financial interests.

For instance, a creditor might object if the new car payment looks way too high for your post-bankruptcy budget, raising red flags about your ability to manage finances.

This review period is a critical safeguard. It ensures that all parties agree the transaction is fair and doesn't improperly remove value from the bankruptcy estate that could have otherwise gone to creditors.

If nobody objects, the judge will usually approve the motion and issue a court order. That official document is your green light, giving you the legal authority to complete the trade. Getting this pre-approval is non-negotiable.

Handling assets after you file is a tricky business, and the rules are strict. You can learn more about the complexities of selling a car after bankruptcy. With bankruptcy filings jumping by 10.6% in the last year, it's clear that a lot of families are trying to navigate these exact rules.

Why You Absolutely Need an Attorney for a Car Trade

Trying to trade in a car during an active Chapter 7 bankruptcy without legal help is like navigating a minefield blindfolded. The rules are incredibly complex, the stakes are high, and one wrong move could jeopardize your entire financial future.

This isn't just about paperwork. It's a delicate dance between bankruptcy law, court procedures, and the rights of your creditors. One of the biggest pitfalls is accidentally creating non-exempt equity. For instance, you could trade a car that was fully protected for a new one that leaves thousands of dollars in value exposed—money the trustee can and will take.

The Role of a Bankruptcy Attorney

An experienced Athens bankruptcy lawyer does more than just fill out forms. They become your strategist, your advocate, and your shield, making sure your fresh start is secure. Their real value comes from a deep understanding of local court rules and what specific trustees look for when they see a request to trade a vehicle.

Here’s how they protect your interests:

- Strategic Planning: They'll analyze your car’s equity, your available exemptions, and the details of the new vehicle to make sure the deal is solid and legally sound.

- Compelling Arguments: They know how to draft a persuasive legal motion that shows the judge and the trustee exactly why the trade is necessary and fair.

- Managing the Process: Your attorney will handle every single communication with the court, the trustee, and your creditors, dealing with objections and ensuring no deadline is missed.

Trying to do this on your own often leads to expensive mistakes. You could violate the automatic stay, have the court reverse your trade, or even get your entire bankruptcy case dismissed. Professional legal advice isn't just an expense—it's essential protection.

An attorney ensures that when you ask, "can I trade my car during chapter 7," the whole process is handled correctly from the very beginning. They know how to structure the transaction to protect your assets and avoid raising red flags with the trustee.

For more on why protecting your assets is so critical, you can read about the serious consequences of transferring assets before filing bankruptcy in Georgia. The right legal guidance truly is the difference between a smooth trade and a catastrophic mistake.

Common Questions About Trading a Car During Bankruptcy

Filing for Chapter 7 brings up a ton of questions, especially when it comes to something as essential as your car. Let's tackle some of the most common situations people find themselves in when they need to trade a vehicle mid-bankruptcy.

What if My Car Breaks Down After I File for Chapter 7?

Life happens. If your primary car suddenly dies right after you've filed, you might have a real reason for an emergency trade-in. But hold on—you can't just run out and buy a new car.

Your first call must be to your bankruptcy attorney. Immediately.

Your lawyer will need to file an emergency motion with the court. The goal is to explain that you need reliable transportation to get to work and handle your daily life. The key here is proving the trade is a necessity, not just a preference for a newer model. You'll have to show that the new car has similar (or less) equity than the one that broke down, making sure the bankruptcy estate isn't losing any value.

Can I Trade My Car Just Before Filing for Bankruptcy?

This is a huge red flag, and you should absolutely avoid it. The bankruptcy trustee has the authority to review all your major financial moves in the months—and sometimes even years—before you file. This is often called the "look-back period."

Here's the problem: if you trade a paid-off car (an asset that could potentially be sold to pay creditors) for a new car with a big loan, it looks like you're trying to hide assets. In legal terms, this is a fraudulent transfer. If the trustee even suspects this, they can unwind the deal, take the old car back, or—even worse—the court could deny your entire bankruptcy discharge.

Always, always talk to your attorney about any vehicle sales or trades you're considering before you file.

Key Takeaway: Any transaction right before filing that seems to shift value away from your creditors is going to cause serious problems. Full transparency with your attorney from the start is the only way to avoid these complications.

Does Negative Equity Make It Easier to Trade My Car?

Having negative equity—where you owe more on the loan than the car is actually worth—definitely simplifies things, but it doesn't give you a free pass. Since the car has no equity, it holds no value for the bankruptcy estate. This means the trustee is far less likely to object to you getting rid of it.

However, the transaction still involves disposing of estate property and, in most cases, taking on new debt while you're in an active bankruptcy case. Your attorney still has to file the correct motion to get the court's approval for both the trade and any new financing. The judge will want to see that the new deal is reasonable and, most importantly, affordable for you.

Navigating the complexities of bankruptcy requires an expert guide to protect your assets and help you secure your financial future. The team at Morgan & Morgan Attorneys at Law P.C. has over 30 years of experience helping Athens residents regain control. For a clear path forward, visit us at https://morganlawyers.com.

Lee Paulk Morgan

With more than 41 years of experience in the areas of Bankruptcy, Disability, and Workers’ Compensation, Lee Paulk Morgan is one of the most respected Bankruptcy and Disability attorneys in Athens, Georgia. His tireless dedication to serving clients has gained him the reputation of a premier attorney in his areas of practice, as well as the trust and respect of other legal experts, who often refer clients to him.

SHARE

RELATED POSTS

Do Employers Have To Notify Employees Wage Garnishment Georgia: 2026 Guide

Let's get straight to the point: do employers have to notify employees about wage garnishment in Georgia? The short answer is no. Under Georgia law, your employer doesn’t have to give you a separate heads-up…

What Is Cram Down In Bankruptcy: A Georgia Debtor’s Guide

A cram down is one of the most powerful tools you have in a Chapter 13 bankruptcy. It can force a lender to reduce your loan balance to match the property's current value. It basically…